Northmill och NyföretagarCentrum samarbetar för att göra det enklare att starta företag, med särskilt fokus på kvinnor och utlandsfödda entreprenörer.

Northmill Bank utser Julie Chatterjee till VD för att förbättra kundupplevelsen och driva tillväxt.

Ett partnerskap för att stötta Sveriges småföretagare med förmånliga finansiella lösningar.

Privata Affärer applauds Northmill’s fee-free debit card, offering 2% interest savings and innovative financial benefits.

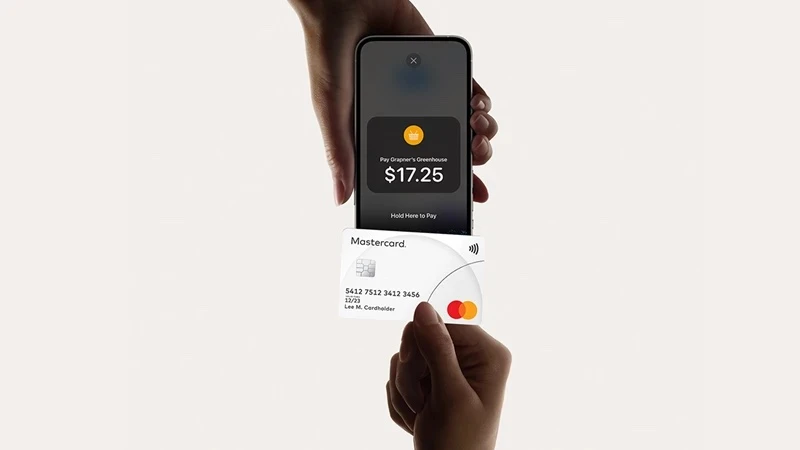

Finaro, Mastercard, Northmill, and NMI launch Europe's first Cloud Commerce solution, enabling contactless payments via smartphones.

Northmill Bank connects to Swish, enhancing its services for over 2,500 business customers.

Northmill explains how source generators simplify coding by automating code production, boosting efficiency for developers.

Northmill launches Apple Pay, offering secure, contactless payments for users via iPhone, Apple Watch, iPad, or Mac.

Northmill boosted its conversion rate by 30% by improving the onboarding process with ThoughtSpot analytics.

First bank to offer personal video calls

Northmill Bank implements React Native to develop platform-agnostic applications, streamlining development and enhancing customer experience.

Northmill acquires Moreflo to modernize shopping experiences, empowering merchants with seamless in-store and online solutions.

How much do skills and experience matter? For Henrik Engström, head of Talent Acquisition at Northmill, there are other important pieces of the puzzle.

Tord Topsholm appointed as Northmill Bank's new CEO to drive growth and take the neobank to the next level.

Northmill Bank appoints Sofia Wingren to the board, bringing experience from MTG and EF Education First.

Northmill Bank launched Reduce in Norway to help customers lower interest rates on existing loans.

What is Event Driven Architecture and how does it help us to scale a Microservice infrastructure? In this deep dive we will try to give you the answers!

Northmill Bank has been granted a Visa Principal license, enabling the neobank to offer customers more control, flexibility, and innovative features.

Jarosław Mutwil prefers not to choose. As a Development Manager at Northmill, he constantly aims to develop himself.

Michaɫ Górski from Poland is responsible for the day-to-day tech-operations, pretty much inspired by Leonardo da Vinci with a modern spirit.

Stockholm, Sweden 30 April 2021 - Northmill Group AB (publ), org. no. 556786-5257.

Northmill Bank implemented Snowflake's Data Cloud, Fivetran, and Matillion in under 12 weeks, enhancing scalability, compliance, and customer experience.

Northmill Bank launches "Power of We" to support women's football in Sweden's divisions 1 to 5.

– The initiative Power of We starts with 32 clubs from Division 1 to 5

Northmill Bank was recognized by Financial Times as one of Europe’s fastest-growing companies for the second year in a row.

For the second consecutive year, Northmill Bank has been recognized by the Financial Times as one of the fastest growing companies in Europe.

By plugging Tink’s account aggregation technology into its app, Northmill will leverage open banking to deliver a seamless and relevant customer experience.

Ana Cancino, software engineer at Northmill Bank, shares her journey from Venezuela to Sweden and her passion for creating customer-focused financial products.

Northmill Bank raises SEK 250 million to fuel European expansion and accelerate new product development.

A product specialist. A plant lover. And a bilingual traveler with a beating heart for a home she never lived in.

A deep-dive from the inside - how we learned the best team setup for our neobank, by Łukasz Wójcik

Northmill Bank introduces a 24-month fixed-rate savings account with state-provided deposit insurance, enhancing its savings product lineup.

Swedish neobank Northmill Bank and the open banking platform Tink, have started a collaboration that will open up new opportunities.

Northmill Bank becomes a member of the Swedish Central Bank's payment system, RIX, enhancing its independence and enabling the addition of new, personalized banking products.

How Northmill Bank creates future conditions for a relevant banking experience

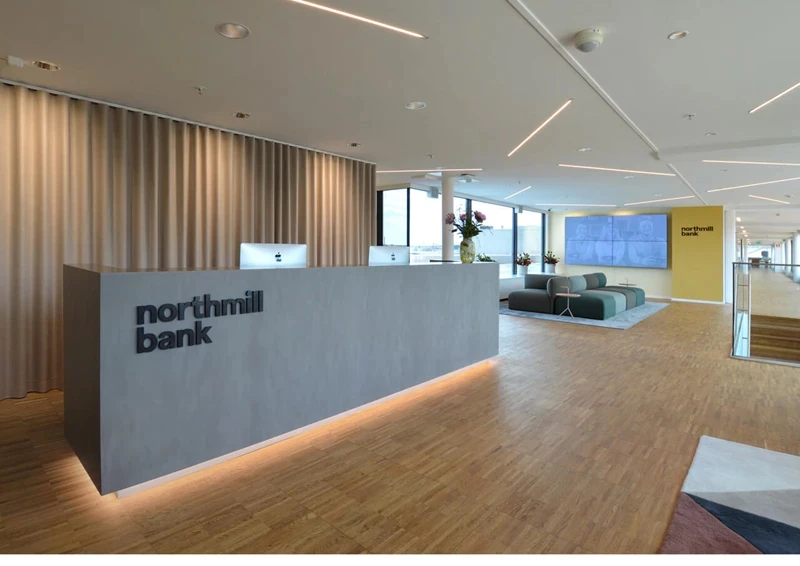

Northmill Bank's "The Power of We" initiative emphasizes a collaborative work environment, integrating employee input into office design to foster innovation and reflect core values.

Northmill, whose mission is to improve everyone's financial life, launches a new product that will lay the foundation for future growth on the Finnish market.

Northmill Bank partners with AWS to enhance scalability, security, and agility, delivering innovative cloud-based banking services.

Northmill Bank celebrates its first anniversary, launching 8 new products, achieving 90% customer satisfaction, and ranking 4th in solidity

Northmill Bank launches tailored customer support in sign language, led by Carolina Agerberg, fluent in sign language.

– Tailoring customer service for 1,4 million Swedes with hearing impairment

Northmill's interim report for January–June 2020 shows a 33% increase in the total credit portfolio to SEK 1,441 million and a 10% rise in net interest income to SEK 168.1 million.

Northmill updates the redemption timeline for 2018/2021 bonds, finalizing on September 11, 2020, before delisting.

In part two of our series with Margareta Lindahl, Northmill Bank Chairwoman, we explore culture's role in the modern economy.

Northmill Group AB redeems all outstanding bonds, ensuring full repayment with accrued interest before delisting

We met up with Margareta Lindahl, Chairwoman of the Board at Northmill Bank, to learn how emerging technology affects leadership and organization in an industry in constant change

Northmill Bank, Sweden’s 4th most solvent bank, uses agile teams and advanced tech to deliver 90%+ customer satisfaction

Northmill Bank broadens its savings offering with a new fixed-rate account, backed by state-provided deposit insurance

Northmill's Q1 2020 report shows a 47% increase in total credit portfolio to SEK 1,598 million and a 29% rise in net interest income to SEK 87.5 million.

Stockholm, Sweden 30 April – Northmill Group AB (publ), org. no. 556786-5257.

Northmill continues its growth journey, attracting top talent to revolutionize the financial industry.

Northmill Group AB (publ) has repurchased additional bonds with a nominal value of SEK 85 million, aiming to improve net interest income

- A vital step to meet all customers on their terms

Financial Times has in its yearly list FT 1000 recognized the Swedish tech bank Northmill as one of the fastest-growing companies in Europe.

Northmill Group AB increased its loan portfolio by 36.6% and invested in IT and product development for long-term growth.

Northmill Bank har för tredje året i rad tilldelats Di Gasell-utmärkelsen av Dagens Industri som ett av Sveriges snabbast växande företag.

Northmill’s interim report for Jan–Sep 2019 shows 26.7% loan growth to SEK 1,285M and a 3% rise in net interest income to SEK 229.4M.

Northmill Bank rekryterar Johan Nordström som Chief Credit Officer för att stärka kredit- och analysavdelningen

Northmill Bank participated in Nordic Tech Day 2019, discussing the development of their cloud-based digital mobile bank and future opportunities.

Northmill's culture is built on CRAFT values: Curious, Relentless, Active, Focused, and Thorough, driving innovation and customer focus.

Northmill Bank received a banking license from the Swedish Financial Supervisory Authority in 2019, enabling the launch of savings accounts, payment services, and cards.

Northmill increased revenues slightly in H1 2019 while focusing on growth investments and delivering a 30% return on equity.

We interviewed our very own security expert and PSD2 specialist, Ninos Gawrieh. And since we had so much to talk about, we decided to split the interview into two parts.

Northmill Group publishes bond prospectus and applies for listing of the bonds on Nasdaq Stockholm

Northmill increased revenues by 42% in 2018 and planned strategic investments to become a licensed bank.

Northmill appoints Daniel Roxo as Chief Risk Officer to strengthen risk management and integrate it into core operations.

January–March 2019 (compared to January–March 2018

Northmill Bank has strengthened its position in Finland by receiving the "Growth Company 2019" and "Achiever 2019" awards from Kauppalehti.

Northmill Bank received the Achiever Award 2018 for strong growth, profitability, and financial stability.

Northmill ökade intäkterna med 58% under januari–september 2018 och utsåg medgrundaren Hikmet Ego till ny VD.

Northmill expands its Board of Directors with the new member Karl Källberg, who brings over 20 years of expertise in risk and analytics from the financial industry.

Niclas Carlsson joins Northmill as Group Legal Counsel, bringing expertise in IT and intellectual property law to strengthen the legal team

Northmill was recognized as one of Sweden's fastest-growing companies in 2018, receiving the Di Gasell award from Dagens Industri.

Northmill partners with Zmarta to offer transparent financial products, enhancing user experience and access to fair services.

Northmill Poland expands, moving to a new office in Silesia Star to support growth and attract top talent.

Northmill is happy to announce that the company has been approved as a Payment Service Provider.

Northmill Group AB (publ) has issued a senior unsecured bond of SEK 500 million, with a total framework of SEK 1,000 million and a 3-year tenor.

Northmill och Trustly samarbetar för att förenkla kreditprocessen och möjliggöra realtidsbetalningar för 200 000 användare

Northmill is happy to announce that Margareta Lindahl has been appointed the company’s new Chairwoman.